Ever wonder why negative gearing benefits are unassailable to the ALP? Or why their response to a housing bubble is to increase the First Home Owners Grant to a boost? Why none of their pronouncements on housing ever make sense? Why Tanya Plibersek as Federal Housing Minister was wont to say, in effect, 'the poor will always be amongst you, so you may as well make them your tenants!'.

Plibersek and the kitchen cabinet were moved to boost the FHOG solely on the request of the head of the REIA when real estate sales slowed down marginally from record highs, driving the Federal budget further into deficit in the process.

Constantly decreasing home ownership stats since 1986 (Hawke and Keating years), especially in lower income households, clearly indicate the ALP have become class traitors. Instead of using government's birds-eye view of the economy to tailor policy to a better outcome than the market can deliver, they instead lie about 'housing shortages' and raid the Treasury coffers to prop up speculative loss-making investors and real estate interests.

Real estate and the ALP

In considering the lack of action by the Victorian Labor government on real estate-related matters (except for allowing developers to now rip 20% off mug buyers), you need to look no further than the rice-paper thin closeness of the REIV and the ALP -- represented by no less than Robert LaRocca, an ALP apparatchik, and present chief lobbyist for the REIV. As well being a former Labor mayor, LaRocca was an adviser to a consumer affairs minister (Marsha Thomson) -- and had direct influence over that agency. The very agency responsible for overseeing the real estate industry -- Consumer Affairs Victoria.

An agency deeply compromised by its close relationship with the ALP, its director proudly spruiking her close relationship with various ALP MPs and a couple of ex-ministerial staffers now working within the agency. It's more a branch of King Street than Treasury Place.

http://www.crikey.com.au/2010/09/23/tips-and-rumours-318/

Home ownership fall will pressure welfare

People over 65 in Sydney now enjoy an 82 per cent home ownership rate, but the proportion of lower-middle income households in Sydney without their own home rose from 26 per cent to 40 per cent in the 45-to-64 age group between 1986 and 2006.

''The substantial loss of home ownership by this age group was concentrated where it is likely to have the worst welfare outcomes as the group ages,'' an Australian Housing and Urban Research Institute study reported.

''They can expect a very long period of private rental under reduced circumstances.''

In 1986, about 60 per cent of middle-income households headed by people aged 25 to 44 owned their own home. By 2006 about 45 per cent were home owners.

There were now 217,000 fewer Sydney home-owning households in the 25-to-64 age group than if the tenure incidence levels of 1986 had been preserved.

Sydney's overall home ownership rate sat at 67.2 per cent in 2006, down on the 70.3 per cent level in 1986.

The report concluded the benefit of higher household incomes between 1998-2007 went into pushing up house prices and debt rather than improving home ownership equity or increasing the stock of housing.

''The very high housing prices that are currently extant are a major concern. It is our contention that this situation has been caused by government action - a deregulation of finance in the 1980s with no corresponding deregulation of planning.

''High house prices act as a drag upon growth and competitiveness, have exaggerated inequities in wealth and intergenerational inequity, and they will eventually increase the welfare burden.''

http://www.smh.com.au/business/property/home-ownership-fall-to-pressure-welfare-20100919-15hyt.html

Friday, September 24, 2010

Thursday, January 01, 2009

A couple of announcements

Australian bailout of dodgy banks

(and I thought we were 'decoupled' from the international maelstrom in the US, UK and now Europe)

The Australian Federal government is doing its very own version of the US bank failure bailout with taxpayer's money, so it can keep the Ponzi scheme going a bit longer and stop market prices for housing correcting somewhere back to where they should be.

Dan at bubblepedia.net.au has sent the following note:

There is also a lot of treatment of the bailout at the Australian forum of the Global House Price Crash site.

Affordable housing competition

There's a competition to produce a 3 minute film of anything to do with 'busting the myths of the housing crisis' from the incredibly busy and energetic team at Earthsharing Australia. I'm very late announcing this competition here, apologies, and I haven't had time to put in a contribution either, unfortunately. However, any quality will do, down to a mobile phone camera...

(and I thought we were 'decoupled' from the international maelstrom in the US, UK and now Europe)

The Australian Federal government is doing its very own version of the US bank failure bailout with taxpayer's money, so it can keep the Ponzi scheme going a bit longer and stop market prices for housing correcting somewhere back to where they should be.

Dan at bubblepedia.net.au has sent the following note:

There is a bailout happening right now under our noses for the gamblers. I object in the strongest possible terms to wasting my tax dollars to pay the gambling debts of our own sub prime lenders in an attempt to keep the bubble going for just one more electoral term.I'm trying to get people writing and shouting here: http://bubblepedia.net.au/tiki-view_blog.php?blogId=9

There is also a lot of treatment of the bailout at the Australian forum of the Global House Price Crash site.

Affordable housing competition

There's a competition to produce a 3 minute film of anything to do with 'busting the myths of the housing crisis' from the incredibly busy and energetic team at Earthsharing Australia. I'm very late announcing this competition here, apologies, and I haven't had time to put in a contribution either, unfortunately. However, any quality will do, down to a mobile phone camera...

We are working on a film competition right now called "I Want To Live Here"- it's a call out to those feeling disenfranchised or 'fenced-out' of the housing market to bust the myths of the housing crisis. We want people to share their stories, explore the causes and effects of the housing crisis and speculation into a 3-minute film of any genre or style.

The winner will receive a $3000 cash prize.

The Top 3 film will be shown at an Official screening and the winner announced in early December. Entries are Open now until October 2nd.

Regards, Mia

--I Want To Live Here Film Competition — Bust the myths of our Housing Crisis--

Earthsharing Australia

HQ: 1/27 Hardware Lane, Melbourne 3000

Ph: (03) 9670 2754

http://www.iwanttolivehere.org.au/

Wednesday, December 31, 2008

Statement concerning the failure of governments to govern

With regard to watching the housing 'boom' unfold without oversight, disenfranchising the next generation, we can only accuse governments of callousness and indifference, if not rampant profiteering wherever possible.

Housing and the real estate industry has become a giant Ponzi scheme, and governments are happy to simply sit back and observe — when they're not busy selling off Crown land to the highest bidder themselves and taking increasing stamp duties to plump up their coffers. With rising interest rates and property already hugely overvalued in Australia, we are about to witness a train wreck in slow motion as the Ponzi scheme comes off the rails.

Well paid but highly unimpressive ministers, advisers and public servants fail to see the economic chain of cause and effect caused by allowing speculation in housing and land to run rampant. Lowering interest rates to stimulate the economy (often after a stock market crash, also caused by speculation) only leads people to irrationally pour capital into housing instead, elevating prices well above sensible returns on investment, and denying affordability to many, causing a failure of the social settlement. High mortgage repayments lead price setters such as shopkeepers to elevate their prices to cover their living costs. (However, high mortgage repayments also cause consumers to draw back from making purchases.) The higher cost of everything eventually causes industrial unrest and disruption and wage inflation, and eventually sparks a spiral of general inflation. The response is to push interest rates up again, causing more damage to home budgets and businesses. Nobody's quality of living has gone up except for real estate industry workers and the empty nesters who cashed out their homes. Meanwhile, governments keep taking things out of the CPI calculation to try to keep wages under control by hiding the real size of inflation. For some reason, you don't seem to get this story anywhere, not from the Reserve Bank, not from Treasury.

CHIRS - Community Housing Online:

With regard to the politicians, with their 2 year longview on everything:

Housing and the real estate industry has become a giant Ponzi scheme, and governments are happy to simply sit back and observe — when they're not busy selling off Crown land to the highest bidder themselves and taking increasing stamp duties to plump up their coffers. With rising interest rates and property already hugely overvalued in Australia, we are about to witness a train wreck in slow motion as the Ponzi scheme comes off the rails.

Well paid but highly unimpressive ministers, advisers and public servants fail to see the economic chain of cause and effect caused by allowing speculation in housing and land to run rampant. Lowering interest rates to stimulate the economy (often after a stock market crash, also caused by speculation) only leads people to irrationally pour capital into housing instead, elevating prices well above sensible returns on investment, and denying affordability to many, causing a failure of the social settlement. High mortgage repayments lead price setters such as shopkeepers to elevate their prices to cover their living costs. (However, high mortgage repayments also cause consumers to draw back from making purchases.) The higher cost of everything eventually causes industrial unrest and disruption and wage inflation, and eventually sparks a spiral of general inflation. The response is to push interest rates up again, causing more damage to home budgets and businesses. Nobody's quality of living has gone up except for real estate industry workers and the empty nesters who cashed out their homes. Meanwhile, governments keep taking things out of the CPI calculation to try to keep wages under control by hiding the real size of inflation. For some reason, you don't seem to get this story anywhere, not from the Reserve Bank, not from Treasury.

CHIRS - Community Housing Online:

With regard to the politicians, with their 2 year longview on everything:

The main barrier to progress appears to be that housing continues to lie off-centre from the main economic, social and political concerns of governments at all levels. In part, this involves an inertial lag effect. For most of the post-War period, the vast majority of Australians have been well housed by historical and international standards. Housing, labour and financial markets worked together to ensure that housing standards were adequate or better for perhaps 85 per cent of the population. A similar proportion of the population became home owners at some time during their lives. The fact that this dominant housing career and expectation has broken down over the past 20 years appears to have eluded many policy makers, who still look to the housing market operating within conventional parameters to meet housing needs for all but a tiny residualised group in the population.

It is this dominant view—along with the tendency to uncritically celebrate house price inflation as a sign of a healthy economy and domestic world—that needs to be taken head on by people concerned with both Australia's long term economic sustainability and the immediate social problems of declining housing affordability for an increasing number of Australians.

Show me the money: financing more affordable housing - Mike Berry

While it lasted, the boom added substantially to the wealth of existing home owners, but it has made home ownership more expensive for aspiring new buyers. In its aftermath, three questions arise. First, who financed the capital gains that home owners have enjoyed? Second, has home ownership become unaffordable for the younger generation? And third, what, if anything, should the government be doing to help young families get onto the home ownership ladder?

Rapid house price inflation also has wider economic costs, for it can distort the way we use capital. The Productivity Commission notes how, ‘Rising prices can create expectations of further price increases, unrelated to any change in market fundamentals. Young workers rush to take out huge mortgages before house prices spiral out of reach, and older buyers are seduced into investing in rental property while disregarding falling rental returns. Panic buying creates a housing ‘bubble’ which sucks money out of productive investments and eventually threatens the whole economy.’Just as damaging in the long-term are the sociological effects of high house price inflation. The longer a housing boom goes on, the more it is likely to foster what Max Weber called a spirit of ‘booty capitalism’ emphasising pursuit of short-term windfall profits at the expense of hard work, thrift, enterprise and long-term planning. When passive ownership of a house delivers riches far beyond what most people could accumulate from many years of working and saving, traditional virtues emphasising hard work, saving, enterprise and deferred gratification are likely to get eroded, yet these are values on which capitalist liberal democracy ultimately depends. Savings, certainly, have been in free-fall. The household savings ratio, which was 10% in 1990, is now negative, and debt servicing is costing an average of 9% of personal incomes.

After the House Price Boom - Is this the end of the Australian dream? - Peter Saunders

Causes of the housing boom

There have been a number of secular trends in recent decades around household formation and income which have combined to drive up housing prices excessively, and, I hope, unsustainably. These include:

- greater female participation in the workplace, leading to many more double income families, coupled with free market bidding for housing based on what lenders will lend the individual, not what individuals need

- smaller family sizes, possibly partly due to greater workforce participation, individual preference, and so on - partly in order to guarantee a better quality of life for individual children

This has been combined with the continuation of rampant free market commodification of residential property for citizens, where government deliberately keeps out of residential real estate pricing, leaving it to a bidding process in the open market, but reaping enormous stamp duty dividends, land tax and Council rates as a result.

These free market conditions include:

- the sudden liberalisation of credit at a higher risk profile for the banks and other lenders; rise of the NBLs (non-bank lenders) and lo-docs/subprime loans; greater use of interest only loans; and the equalisation of interest rates on loans for investment properties and PPORs (principal places of residence)

- present low interest rates, which are now steadily increasing to fight 'inflation', a good percentage of which has been caused by overheated housing prices

- the advent of 'spruikers' promoting get-rich-quick schemes based on speculative and exploitative behaviours in the property market, and maximising tax breaks, especially 'negative gearing' in the Australian case — see http://www.jenman.com.au/ for examples

- the capitalisation of high stamp duty, and other government levies and charges, into the cost of housing — the 'ratchet' effect

- increasing desperation of purchasers, leading to more inflation and a hysteria effect — à la the Dutch 'tulip boom'

- irrational exuberance of speculative investors (yes, just like in the Great Depression, the dotcom 'tech wreck' and numerous other housing bubbles in the last century which have all ended badly); belief that future infinite capital gains will bail them out for high prices and ongoing losses now. See Steve Keen on 'Minsky's Financial Instability Hypothesis' as a counter to the neo-classical 'equilibrium theory' of markets - http://www.debtdeflation.com/blogs/2008/03/10/time-to-read-some-minsky/

- plenty of developers, real estate agents and baby boomers highly prepared to cash in on this desperation and greed

- the permeability of the real estate market to other markets as an investment vehicle, and relatively low costs of purchase compared with other countries

- very few protections for owner-occupiers in terms of cost controls, except the limit of what the market will bear

- in Australia, very generous negative gearing rates for investors compared with other countries, where housing investment losses are offset against all income, not just income from the property, meaning that the Tax Office is happy to be an equal partner in any loss for top bracket income earners.

Unfortunately, every single spare cent in households then becomes 'capitalised' into purchasing real estate, in a bidding war between couples and investors, both long-term and speculative.

Policy suggestions for more affordable housing

My policy suggestions designed to make housing more affordable in Australia and limit the effects of a rapacious, destructive boom include (and are by no means limited to):

A price correction is needed, and governments must provide affordable places whether or not real estate prices in the open market crash in the next few months and coming years or not.

It appals me that governments instead are willing to attempt to profiteer from these inflated prices by selling prime land and taking excessive stamp duties at the top of an unsustainable capitalist price wave. And, as we know, the whole house of cards is now tumbling down starting with the collapse of mortgage derivatives in the US that fed credit into the rest of the OECD, with a credit freeze and the disappearance of billions in non-existent 'value' off assets and derivatives.

- requirement of at least 33% of new development to be 'affordable' properties, rather than the current paltry 3% set by state governments — these higher rates are the norm in the UK and France

- PPP developments and partnerships sponsored by government on state, Crown and ex-Defence land – and involving more partnerships with SME construction firms than with big players, thus cutting out fat developer profits, and land speculation profiteering

- release of Defence, State and Crown lands for responsible, affordable, environmentally sustainable development, e.g. disused hospital sites, ADF bases, RTA land, empty land and so on, with price covenants on developments

- control and lowering of land costs where owned by the state or Federal governments, which have an arbitrary value anyhow, rather than selling off land willy-nilly to the highest bidder to plump up state and Federal coffers

- setting long-term price covenants on developed affordable properties under the above regimes, indexed only to CPI or median wage increases, and an at-cost-only allowance for any further renovation value added by owner-occupiers (as assessed by a valuer)

- boosting and improving the stock of both 'public' housing and 'social housing', i.e. cost-controlled housing as described above. Labor Ministers such as Mark Latham and Cherie Burton benefited from this sort of housing growing up, but it has been abandoned more recently due to eco-rat market principles infecting government.

- creation of leasehold titles to be held in perpetuity by government, with the intention of controlling the selling prices of properties developed on them, and to ensure responsible control is retained over the land — this may be an inferior approach to the above approaches

- bypassing/removal of real estate agents and associated advertising charges and hefty commissions in selling these properties, given that they will shift without the need for an agent, and that agents' fees contribute to the 'ratchet effect' in housing

- stamp duty and other transaction cost waivers on these properties, similar to NSW 'HomePlus' scheme for first home buyers

- levy a land tax on unused property in urban areas – this tax could be allocated at local government level, to be returned to cash-strapped Councils. The tax would serve as an inducement to sell up rather than hoard disused land and property, both on small and large scales — see the oligopoly of developers and use of land banking to control supply as yet another factor. Gough Whitlam showed courage and broke up this cartel in the 70s, today's Labor are too compromised to address the issue.

- streamlining approval processes with local Councils for new construction (this is one of the more minimal suggestions currently put forward by state and Federal governments, so that they can blame someone else for the problem)

- lobby Federal Government to stop negative gearing breaks and capital gains tax concessions for investors and implement workable incentives towards home ownership which do not go on to further inflate housing prices; or else the implementation of policy and legislation to offset existing destructive arrangements by the Federal Government. For instance, negative gearing breaks could be quarantined to apply only to rental incomes, not total personal income, as in the UK and the US.

- resumption of land if necessary, e.g. to unite two blocks with a small title between them, or to reclaim an unused or underused site from an unwilling vendor in the public interest. The non-negotiable offer of discounted prices to large vendors such as at the CUB brewery site at Ultimo, Sydney. They have profited enough from the drinking habits of the working class over nearly two centuries – it's time to put something back. It's interesting that the land at Kurnell was going to be 'resumed if necessary' for the now shelved desalination plant – very tough-talking stuff when it comes to projects like that, but nothing in housing? The RTA is always resuming land to put through new freeways, using its extensive powers.

- the passing of legislation and creation of taxes to control land prices and prevent capitalist boom/bust waves and discourage speculative activity in property, to 'nationalise' the sale and pricing of property to some extent, to curb and keep real estate agents in check in any number of ways with stiff penalties (including making inflationary and misrepresentative claims of unlimited capital growth to gullible purchasers, encouraging the creation of endless 'investment properties', REI media announcements to this effect) and banning unethical practices to allow for decent affordable owner-occupied housing. Allowing the sale of rental properties only for the use of itinerant workers, visitors, and overseas students, etc. (More decent and affordable accommodation needs to be created for overseas and local students also to reduce current apartment overcrowding problems – currently there are 2 and 3 bedroom apartments all over the city containing up to 10 overseas students.) Better inclusionary zoning and affordability measures around the capital cities to allow ordinary workers to live in the vicinity of their work, thus solving some of the transportation problems of the city and improving social capital.

- stop bun-fighting and buck-passing across the tiers of government, and take ownership of the problem at all levels. It's ludicrous to expect individual councils to manage housing affordability individually with limited powers and resources and with no holistic plan across the city and state, to say nothing of the pecuniary conflicts of interest which appear with monotonous regularity.

A price correction is needed, and governments must provide affordable places whether or not real estate prices in the open market crash in the next few months and coming years or not.

It appals me that governments instead are willing to attempt to profiteer from these inflated prices by selling prime land and taking excessive stamp duties at the top of an unsustainable capitalist price wave. And, as we know, the whole house of cards is now tumbling down starting with the collapse of mortgage derivatives in the US that fed credit into the rest of the OECD, with a credit freeze and the disappearance of billions in non-existent 'value' off assets and derivatives.

Monday, December 31, 2007

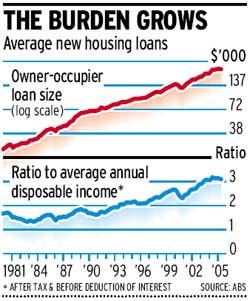

Is household debt getting worse?

Even though home prices have stopped rising in most parts of the country, household debt continues to grow.

The ratio of household debt to income has reached a record 150 per cent - one of the highest in the world - and the ratio of house prices to disposable income is also very high by historical and international standards.

The share of households with debt secured on their home is rising, having jumped from less than 30 per cent in the mid-1990s to 36 per cent.

"The household sector remains vulnerable to a deterioration in the economic climate, and there remains a possibility that the adjustment could turn out to be much larger than currently anticipated," the report said.

Is household debt getting worse?

Note how spiralling housing costs have fed into the national debt, creating an unproductive international debt to service.

Note also that many small retail businesses are going to the wall, as disposable income is at an all time low.

What does the NSW Labor government and Australian federal Government do about it? Nothing, of course... It's far easier and politically correct to be laissez-faire and eco-rat (while still dashing off important-sounding polished speeches about nothing) and let new and prospective homebuyers (and the macro-economy) suffer.

Monday, December 03, 2007

Saturday, November 24, 2007

Mortgage stress may be behind Bible belt crime

Quelle surprise:

SYDNEY'S Bible belt is known for its McMansions, aspirational voters and enthusiastic church-goers. But the conservative, affluent Hills District is also in the grip of a crime wave - and mortgage stress may be behind it.Mortgage stress may be behind Bible belt crime - National - smh.com.au

Over the past four years, Baulkham Hills Shire has experienced rising rates of violence and robbery. Domestic violence has risen by almost 20 per cent, assault is up by almost 10 per cent and harassment by 23 per cent.

There have been five murders in the past two years; there were none in the five years before that. They include the stabbing murder of Richard Carruthers, the 36-year-old redesigner of the Olympic cauldron, in his Castle Hill home. Three of the murders remain unsolved.

Many families in the area are also struggling financially, which can influence domestic violence statistics. "What you have in the Hills District is more people paying more off home loans than the rest of Sydney," Dr Lee said.

"You've got 50 per cent of home owners paying more than $2000 a month off a home. That's at least 10 per cent more than the average. I'm not saying it's causal, but I think it's an interesting figure."

The Local Area Commander, Superintendent Sue Waites, also suggests a link between financial stress and domestic violence. Domestic violence problems could also be fuelling the 23.2 per cent rise in harassment, threatening behaviour and private nuisance charges. "[Incidents] include sending inappropriate text messages to persons via mobile phones," she said.

Saturday, November 03, 2007

Tale of two Sydneys as property divide widens

SYDNEY'S two-speed property market could continue this year as mortgagee-in-possession sales drag down the lower end of the market.

An Australian Property Monitors rating of the growth of property values of about 700 suburbs in 2006 shows the city's affluent enclaves surged ahead, while areas in the west and south-west languished.

Tale of two Sydneys as property divide widens - National - smh.com.au

Tuesday, October 09, 2007

Sydney not alone in seeking housing crisis solution - National - smh.com.au

hmm, Jess Irvine hasn't done a market-pumping piece funded by the REI for a change -- remarkable... As per the article, if politicians want policy suggestions, just come to this site. They are looking at releasing urban Defence land as well as the State and Crown lands, to answer the vexed 'where will the land come from?' question...

Sydney not alone in seeking housing crisis solution

Sydney not alone in seeking housing crisis solution

Wednesday, October 03, 2007

Rent crisis taking psychological toll

THE rental crisis is having negative psychological effects on tenants, with a growing number reporting rent-associated depression and anxiety.

About one in three Australians rent and the survey by realestate.com.au showed 89 per cent of renters reported experiencing negative psychological effects directly related to the rental climate.

Fifty-nine per cent of renters expressed "anxiety" over their renting predicament. Forty-one per cent felt "helpless" in their rental situation and one in five said they felt rage and fury over their situation.

Only 11 per cent of renters are happy with their current accommodation and only 4 per cent feel well cared for by their landlords, the survey found.

But even with a shortage of good accommodation and rents rising by 9 per cent during 2007, the majority of respondents said they would rather stay in less than ideal rental properties then go back into the market.

Fifty-six per cent of prospective tenants were deterred from applying for properties based on the number of people at inspections. More than a third said they felt they would never be able to own a home.

Rent crisis taking psychological toll | The Daily Telegraph

About one in three Australians rent and the survey by realestate.com.au showed 89 per cent of renters reported experiencing negative psychological effects directly related to the rental climate.

Fifty-nine per cent of renters expressed "anxiety" over their renting predicament. Forty-one per cent felt "helpless" in their rental situation and one in five said they felt rage and fury over their situation.

Only 11 per cent of renters are happy with their current accommodation and only 4 per cent feel well cared for by their landlords, the survey found.

But even with a shortage of good accommodation and rents rising by 9 per cent during 2007, the majority of respondents said they would rather stay in less than ideal rental properties then go back into the market.

Fifty-six per cent of prospective tenants were deterred from applying for properties based on the number of people at inspections. More than a third said they felt they would never be able to own a home.

Rent crisis taking psychological toll | The Daily Telegraph

Thursday, September 06, 2007

Credit squeeze hits Aussie banks

There you have it -- the banks opened up the credit floodgates 5 years ago, precipitating the boom, and now it's come full circle -- massive levels of foreclosure, housing inflation, indebtedness, borrowing and consumer risk, so they turn tail and restrict credit again. Of course, 'the gummint is managing the economy'. At least APRA could have done something, but they did very little -- it took an international credit squeeze to stop the local largesse.

This could bring down house prices, because

1) people can borrow less, thus reducing bid prices

2) they will probably also have to pay more interest, also reducing how much they are prepared to pay for housing.

Credit squeeze hits Aussie banks

This could bring down house prices, because

1) people can borrow less, thus reducing bid prices

2) they will probably also have to pay more interest, also reducing how much they are prepared to pay for housing.

Credit squeeze hits Aussie banks

Tuesday, August 28, 2007

Victoria pulls ahead

So cheaper Victoria is pulling ahead of property price-gouging NSW -- and yet heightened demand in Victoria isn't escalating house prices through the roof! Very interesting.

Victoria pulls ahead

NSW is losing the economic race to Victoria, with residents fleeing high property prices and dragging down the state's economic growth.

About 25,000 NSW residents leave for other states and territories every year. And the exodus is constricting the state's economy, with NSW slipping behind its southern neighbour, new analysis by the ANZ's head of Australian economics, Tony Pearson, shows.

Mr Pearson said the Victorian economy had grown twice as fast as NSW's in the last two years, in part due to demographic factors.

"What stands out is the much poorer economic performance of NSW against its peers, particularly relative to Victoria."

Victoria pulls ahead

Monday, August 13, 2007

Housing affordability hits new record low

Those hard-working pollies who 'manage the economy' (or so they keep telling us) are at it again, fixing up the housing affordability problem. Anyone would think they just swanned around for a living delivering speeches, attending openings and taking credit for other people's work, and playing political games with developers, big business, and anyone else with loads of cash. The key words are 'tangible policy action':

Housing affordability hits new record low

"The Australian economy is performing well yet an increasing number of Australians are now being left behind as the degree of housing stress being felt by both mortgage holders and renters continues to intensify," Dr Silberberg said.

"The longer we go without tangible policy action, the worse the situation will become, and that's without higher mortgage rates."

Housing affordability hits new record low

Thursday, August 09, 2007

Ten's company: what the rental squeeze means for owners

More on the housing/renting/apartment overcrowding debacle -- this is what happens when you leave housing in a capitalist free market with laissez-faire politicians 'running' the country -- out and out exploitation of overseas students, rampant unaffordability, and horrible life experience. When was it decided Australia was the land of the 'fair go', and by whom, particularly since it has become populated with property developers and landlording piranhas, the 'fair go' mums and dads of yesteryear.

Ten's company: what the rental squeeze means for owners

Ten's company: what the rental squeeze means for owners

Wednesday, August 01, 2007

Home ownership now an 'unattainable dream'

HOME ownership has become an unattainable dream for many low- to middle-income earners in Australia, a new report has found.

The Beyond Reach report, undertaken by the Residential Development Council (RDC), examines the cost of owning or renting a house or unit for six household “types”, comprising different family and wage structures, in 16 metropolitan locations across the country.

It shows owning a median-price home in almost any location in Australia requires a combined household income of about $100,000, while the average annual wage for workers is $55,000 a year.

According to the report, not one of the 16 locations studied offered a median-priced home that was affordable on that level of income.

In calculating affordability, the report used two different measures - that no more than 30 per cent of household incomes should go on housing costs, and a property should cost no more than three to four times the median household income.

RDC executive director Ross Elliott said the research provided a more human angle on the affordability crisis.

“If key workers necessary for society and the economy to function are being denied entry to the housing market, or if the option of a single income family is now completely shattered by the price of housing, we are faced with obvious long-term social and economic consequences,” he said.

Home ownership now an 'unattainable dream' | The Daily Telegraph

Tuesday, July 31, 2007

Sunday, July 15, 2007

THE POLITICS OF AFFORDABILITY

A great public service article on Neil Jenman's website (www.jenman.com.au), written by Terry Ryder. A fantastic synopsis, well worth reading in its entirety:

THE POLITICS OF AFFORDABILITY

It's almost tragic watching politicians and media puzzling over the two-speed property market and the related issues of low housing affordability and record home repossessions.

The reasons are quite simple.

The common factor pervading these issues is this: Australia's economy is booming but the spoils aren't being evenly shared.

Most of the benefits of the resources-inspired prosperity are being gobbled up by the upper echelons. While the top end is rolling in cash, the average person is no better off than five years ago.

The business elite have never had it so good. Record company profits, generous executive salary packages and a buoyant sharemarket mean those at the top have more dollars than ways to spend them. This is driving the rise and rise of the top end of the residential property market.

But down in the real world, the mainstream where 90% of Australians live, the market is going nowhere fast.

More and more households cannot afford to buy a home, those who already own one are struggling with their mortgages after eight consecutive interest rate rises and banks are repossessing homes at record levels.

The wages report shows that over the period of the economic boom wages have grown at roughly 2% to 3% a year. In other words, not much above the inflation rate. The report states that a significant proportion of households have seen no "real" (after inflation) increase in their incomes over the past five years.

But in the same time frame property prices have doubled in many areas and there have been multiple rises in interest rates.

The problem is this: the typical price has risen a lot, thanks for the recent market boom, and the typical monthly payment has risen greatly also, thanks to all those interest rate rises from the Prime Minister who promised they wouldn't rise if we re-elected him – BUT household incomes haven't kept pace, thanks also to that same Prime Minister who has devoted his life to keeping wages down.

In the property booms of the 1970s and 1980s, prices rose a lot and interest rates were high, but incomes were rising at 8%-9% a year, so affordability didn't suffer too much.

Today, the growing gap between the income needed to get a loan and the actual income earned by the average family is the reason why affordability is at all-time lows – and why we have this strange two-speed property market.

You'll notice that there's no mention in the affordability equation of stamp duty or land supply.

This is a surprise because the development lobby has been desperate to convince us that affordability could be solved overnight if state governments lowered stamp duty and raised the supply of land for new residential development.

It's nonsense but they keep saying it because they have a vested interest in lower stamp duty and higher land supply.

So why is this deception not widely known?

Part of the answer is that media doesn't do its job. There was a time when journalists were proactive in investigating major issues like affordability. Today many journalists simply regurgitate the spin-doctored views of politicians and business lobby groups.

THE POLITICS OF AFFORDABILITY

A housing illusion we buy every time

A reasponable attempt at an analysis of the boom. I particularly like the reference to the stupidity of the sheeple in the following opening quote:

A housing illusion we buy every time

The question is what are the politicians going to do to make homes affordable again? Bring down the price of land? Develop huge tracts of Crown and State land themselves affordably and put price cap covenants on them going forward?

It happens after every housing boom - people go from congratulating themselves on the huge rise in the value of their home to wondering how on earth their children will afford homes of their own. So I've no doubt Kevin Rudd is on a winner with his efforts to focus attention on the deterioration in affordability for first home buyers.

A housing illusion we buy every time

The question is what are the politicians going to do to make homes affordable again? Bring down the price of land? Develop huge tracts of Crown and State land themselves affordably and put price cap covenants on them going forward?

Mortgage stress to hit home at election

Enough said. (And Jessica Irvine at the SMH is not running a RE industry market-pumping story for a change, very strange, what could have lead to this change of heart?)

Mortgage stress to hit home at election

MORE than a third of NSW families with a home loan live in a state of 'mortgage stress', devoting more than 30 per cent of their gross income to mortgage repayments.

This is a massive increase since the 2001 federal election, when the proportion was less than a quarter. Mortgage stress has since risen in every NSW electorate, unpublished census figures show. As housing affordability firms as an election issue, the figures reveal the high level of financial stress confronting many families.

At the same time, buyers are finding it increasingly difficult to get into the market. A survey of 1000 first-home buyers by mortgage broker Mortgage Choice found almost one-third did not expect to buy a home until they were aged 40 or over, and fewer than two in five expected to have secured a home before 30.

NSW is home to the greatest mortgage pain - the figures show 33.2 per cent of families with a home loan live in mortgage stress.

Mortgage stress to hit home at election

Home loans on tap: no deposit, no inspection

Is this somehow connected to the housing boom that the politicians are so earnestly wringing their hands about in Darwin at the Premiers Conference? What to do, what to do?

Home loans on tap: no deposit, no inspection

THE mortgage stress crisis is being worsened by the boom in easy credit, with lenders approving loans without inspecting properties, offering large amounts to borrowers who have no deposit and encouraging buyers to take on debts that would eat up half their income.

Amid concern over the growing practice of loans being approved with no on-site inspection, the Herald discovered yesterday how easily customers can be seduced by quick and simple access to credit.

Home loans on tap: no deposit, no inspection

Sunday, July 01, 2007

Housing costs squeeze budgets

SOARING housing costs are squeezing family budgets in Sydney, even though incomes in the city are higher than almost everywhere else in the country, figures from the 2006 census show.

Mortgage repayments in Sydney are 40 per cent higher than the national median and rents 31 per cent more, even though incomes in the city are only 12 per cent higher.

Housing costs squeeze budgets

Mortgage repayments in Sydney are 40 per cent higher than the national median and rents 31 per cent more, even though incomes in the city are only 12 per cent higher.

Housing costs squeeze budgets

BIS warns of Great Depression dangers from credit spree

Here comes the fallout from easy credit and borrowing — see the following post concerning the increasing number of foreclosures taking place.

BIS warns of Great Depression dangers from credit spree

The Bank for International Settlements, the world's most prestigious financial body, has warned that years of loose monetary policy has fuelled a dangerous credit bubble, leaving the global economy more vulnerable to another 1930s-style slump than generally understood.

"Virtually nobody foresaw the Great Depression of the 1930s, or the crises which affected Japan and southeast Asia in the early and late 1990s. In fact, each downturn was preceded by a period of non-inflationary growth exuberant enough to lead many commentators to suggest that a 'new era' had arrived", said the bank.

The BIS, the ultimate bank of central bankers, pointed to a confluence a worrying signs, citing mass issuance of new-fangled credit instruments, soaring levels of household debt, extreme appetite for risk shown by investors, and entrenched imbalances in the world currency system.

In a thinly-veiled rebuke to the US Federal Reserve, the BIS said central banks were starting to doubt the wisdom of letting asset bubbles build up on the assumption that they could safely be “cleaned up” afterwards - which was more or less the strategy pursued by former Fed chief Alan Greenspan after the dotcom bust.

BIS warns of Great Depression dangers from credit spree

Surge in families forced to sell their homes

Looks pretty grim for the economy, for families, and for the housing boom. Naturally the politicians who pride themselves on 'managing the economy' when times are good (which is an outright lie anyhow at any time) shut up when this sort of thing happens. Never mind that half the reported GDP growth of recent years has been empty inflationary lending on housing at high, unsustainable prices.

Surge in families forced to sell their homes

HUNDREDS of families have been forced to sell their homes, or lenders have repossessed and auctioned them, in Sydney's west and south-west in the past year, property experts say.

There were a record 1400 auctions in the region in the year to March 31, nearly double the number in 2005, Australian Property Monitors figures show.

Michael McNamara, an analyst with the company, said the spate of auctions pointed to a big rise in distressed sales and repossessions in the region. Mostly, sellers in Sydney's cheaper property markets were going to auction because they had to, not because they wanted to, he said. "The big rise in the number of auctions isn't because the market is going well," he said.

"It's jumped because auctions are the preferred method of sale of trustees in bankruptcy and mortgagees in possession. I think that's a very disturbing figure."

The median price for an auction in south-western Sydney in the March quarter was $318,000, $22,000 less than the overall median house price in the region.

"This just brings home the fact that most of these are distressed sales," Mr McNamara said.

Dara Dhillon, the principle of Dhillon Real Estate in Ingleburn, near Campbelltown, said 95 per cent of auctions in south-western Sydney were mortgagee sales. But he said there were many more forced sales where lenders had encouraged borrowers to sell rather than face repossession. "This type of [forced sale] is a big proportion of sales at the moment," he said.

Mr McNamara and Mr Dhillon estimate that hundreds of families in western and south-western Sydney had been forced to sell their homes, or had had homes repossessed and auctioned by lenders, over the past year.

Meanwhile, the total debt burden on Australian households topped $1 trillion for the first time last month, Reserve Bank figures published yesterday showed.

Debt on housing accounts for about 86 per cent of household debt, with the remainder personal debts like credit cards and personal loans. The ratio of household debt to household income has reached 160 per cent, one of the highest in the world. Interest payments now soak up a record 11.9 per cent of household income, nearly three percentage points more than in 1989 when mortgage rates were 17 per cent.

Surge in families forced to sell their homes

Wednesday, June 20, 2007

Blogger learns how to monetise hate

I've spoken to Casey in the past, posted on his website, and *tried* to provide sage counsel to him. Now he's visiting Sydney...

Blogger learns how to monetise hate

Update: I ended up having dinner one night with Casey and chatted about various things. I wanted to help him out more in finding accommodation for a few days, but I'm in the middle of relocating myself, so couldn't offer anything much. Travel broadens the mind...

Blogger learns how to monetise hate

Update: I ended up having dinner one night with Casey and chatted about various things. I wanted to help him out more in finding accommodation for a few days, but I'm in the middle of relocating myself, so couldn't offer anything much. Travel broadens the mind...

Wednesday, April 18, 2007

Rents fuel plight of homeless young

What a surprise that the politicians are doing nothing about housing on their $200K salaries and perks and pensions paid from YOUR money. I thought we were paying politicians to do a job...

Rents fuel plight of homeless young

HOMELESSNESS among people aged under 25 has doubled to 35,000 in the past 20 years, says a commissioner of the first independent inquiry into youth homelessness since an inquiry in 1989.

David MacKenzie, associate professor of sociology at Swinburne University in Victoria, yesterday said youth homelessness now accounted for one-third of all homeless people in Australia.

The problem of homelessness had been worsened by the rental crisis, said the chairman of the inquiry, the David Eldridge, of the Salvation Army. With the pressure on prices forcing out the bottom end of the market, the overflow has been too great for public housing to address.

He said the situation was heightened by governments that favoured the publicity generated by pilot programs over the less 'exciting' job of funding programs that were working.

'The circumstances have all come together at this time to make it a fairly explosive situation,' Major Eldridge said.

Wally Dethlefs, a commissioner who also sat on the 1989 inquiry of Brian Burdekin, a federal human rights commissioner, said: 'It's not just marginalised people, but TAFE and university students ending up in shelters. What we are hearing in this inquiry is [that] because of the increase in rent there is no exit point.'

Rents fuel plight of homeless young

Wednesday, March 21, 2007

Housing Rebounds, Sky Green - Motley Fool

Try not to step in it today, housing bubble watchers. Once again, the real-estate cheerleaders and compliant 'journalists' out there will be trying to put lipstick on the pig with the bogus headline of the day. It will read 'Housing Rebounds,' 'Home Starts Up,' or some other nonsense.

Don't fall for it.

Quick Take: Housing Rebounds, Sky Green [Fool.com] March 20, 2007

Don't fall for it.

Quick Take: Housing Rebounds, Sky Green [Fool.com] March 20, 2007

Monday, March 19, 2007

Media Watch: Front Page - Who's Raising The Rent?

Interesting exposé of the REI and the SMH by ABC's Media Watch, who are increasingly moving to the right these days in their reporting.

Media Watch: Front Page - Who's Raising The Rent? (26/02/2007)

Media Watch: Front Page - Who's Raising The Rent? (26/02/2007)

Monday, March 12, 2007

Housing costs dim appeal of bright city lights

Shared equity schemes are one of the weakest things you can do in terms of reducing land speculation and land bubbles, but we are coming to expect more and more such neo-liberal policies from a Labor party without any real ideas.

Housing costs dim appeal of bright city lights

Poor housing affordability in Sydney, Melbourne and Brisbane had forced an increasing number of first-home buyers to flee the city or remain in regional areas, said Simon Tennent, the association's executive director of housing and economics.

Improved job opportunities in many regional areas - highlighted by the lowest national unemployment rate for 30 years - has encouraged this trend.

'The attraction of the bright lights and the big city, like great job opportunities and that sort of thing, has faded somewhat over the past few years,' Mr Tennent said.

Despite recent weakness in parts of the Sydney housing market, it remains one of the most expensive cities in the world relative to average incomes.

Federal Labor's housing spokeswoman, Tanya Plibersek, said on Friday that a Labor government would consider a federal role in shared equity schemes to assist people on low incomes to enter the housing market.

Housing costs dim appeal of bright city lights

Saturday, March 10, 2007

Seeking Curbed-Cost Appeal, Builders Cut Homes' Price And Size

Why doesn't NSW 'Labor' do affordable housing on state-owned lands instead of selling them off to the highest bidder in an asset sale to try to reduce its half-billion dollar deficit?

Yahoo! Personal Finance

Now that overheated markets such as Miami are cooling fast, Related's talking up another kind of product: affordable homes.

Miami-based Related, the nation's largest condo developer, has trotted out a rebranded "affordable housing division," to build condos for buyers priced out of the market.

The firm has presold 497 of 500 loft condos in a planned downtown Miami high-rise. They're priced from $159,000, about half the median price of existing condos. That's a fraction of the price of many new condos, which often now go unsold.

Related expects to make a return of around 15%. That's about half what its luxury units typically fetch, but the company's not complaining.

"You make less money, but the demand for this type of housing is so great that the volume you can do justifies the concession on the returns," said Oscar Rodriguez, senior vice president of Related's affordable housing division.

Yahoo! Personal Finance

Thursday, February 22, 2007

Why renters fat and thin are singing

It's a pretty safe bet the big story in housing this year will be steep increases in rents. The media have dubbed it the "rent crisis", with a leading property market forecaster, BIS Shrapnel, predicting that rents for inner-Sydney apartments will rise by more than 7 per cent a year for the next five years. But you'll hear worse than that before we're through.

Once again, politicians are going to sit by the sidelines while rents escalate. However, unlike mortgage payments, rentals go into the CPI calculation, and many employers peg wage raises to the CPI. Hence, indifferent, laissez-faire politicians will be watching national inflation spiralling out of control, and there is little interest rate rises from the Reserve Bank will do to fix it. The more interest rates go up to 'control inflation', the more new landlords who paid too much for their property will pass the costs on to tenants, and the more inflation will increase in the community. That's capitalist exploitation of property for you, egged on by the politicians...

Why renters fat and thin are singing

Tuesday, February 13, 2007

Wind out of sales

This shows the incredibly poor quality of urban planning in Sydney — people don't want to live in the far-flung outer suburbs because they are forced to commute huge distances to the city to work. Housing near the city is unaffordable. Housing further out can't be sold. The free-market free-wheeling approach to allocating housing simply isn't working.

Wind out of sales The Daily Telegraph

DEVELOPERS have resorted to offering cash incentives and no-deposit finance as they struggle to sell newly built homes in Sydney's outer suburbs.

Multi-million-dollar housing developments on the city's outskirts have taken the biggest hit, with three rate rises in the past year deterring prospective homebuyers.

Housing Industry Association figures show the number of new houses sold in NSW over the past 10 years has slumped by 50 per cent.

The trend continued last year with 14,121 new homes sold around the country, compared with 14,175 the previous year and 39,860 in 1998/99.

The national figures tell a similar story. Last year, 107,145 new homes were sold, down from 110,979 the previous year.

Half-empty streets and rows of for-sale signs are common at some of the multi-million-dollar estates in outer Sydney as developers turn to lavish gifts and no-deposit finance to attract buyers.

Some estates are offering cash incentives of up to $10,000, no-deposit finance, fixed interest rates or free extras such as air-conditioning.

Only 951 new homes were sold in NSW in December, 2006 - down from about 1127 in December, 2005.

Simon Tennent, executive director of housing and economics for the Housing Industry Association, said Sydney prices were driving young couples and families out of the homebuyer market.

"I'm not surprised (at the fall in NSW), with the price of land in Sydney's growth areas,'' he said.

"And at the end of last year, the three interest rate rises and nerves over other prices, like petrol, just took the wind out of the sails.''

HIA figures show the median block of land in Sydney costs about $325,000 while a similar-sized block in Melbourne costs only $150,000.

"I'm not surprised that some estates are struggling,'' Mr Tennent said. "These are great quality homes on excellent estates, but do the simple maths and you can't afford them.''

The Sunday Telegraph visited several major developments last week. One street in Prestons has 19 houses for sale. At another development site, only 32 of 54 lots had been sold - five in the past four weeks.

Michael McNamara, of Australian Property Monitors, said the new estates had become an unattractive option for those working in the city.

"People just don't want to live there,'' he said. "It's so difficult to get from the outer suburbs of Sydney to the city.''

Wind out of sales The Daily Telegraph

Saturday, February 03, 2007

Housing surge to favour rich

Mr McNamara said that as the three interest rate rises of 2006 took affect, the impact would be felt more deeply by low-to-middle income earners, creating weak property markets in the mortgage belt areas of Sydney, Melbourne and Brisbane.

"Sadly, forced sales will continue to create an oversupply and flat demand in these areas," he said.

The real story is that foreclosures are up, demand at high prices is down, and the boom is over. The bust begins.

(There is no 'surge', just a slight increase in upmarket properties -- largely due to more profits flowing to the top of business in the new environment.)

Housing surge to favour rich

Sunday, January 14, 2007

Harder they fall: Sydney's biggest housing slump

Sydney home prices have suffered their sharpest annual fall on record as the property market continues to slump - and experts are tipping the slide to continue for the next few years.

The price of an average established home in Sydney fell 5 per cent last financial year, the biggest drop since the Bureau of Statistics began keeping records two decades ago.

The results are a far cry from the 20 per cent growth rates during the peak of the property boom, with prices now falling faster than during the recession in the early 1990s.

For Sydney, it is a case of the bigger they come the harder they fall, economists say.

With home prices in the city still about seven times the average annual wage - well above historic ratios of five times typical pay - economists are predicting more falls over the next five years.

Kieran Davies, an analyst with ABN Amro, said: "Given prices are so out of line with wages, it wouldn't be a surprise to see prices remain flat to down for quite a long time - for some five years or longer."

Harder they fall: Sydney's biggest housing slump

Friday, January 12, 2007

Housing not affordable for many workers - Jan. 10, 2007

Americans struggle to afford housing

An annual income of about $85,000 is needed to afford median-priced homes; salaries have not seen modest gains, according to a study.

Saturday, December 30, 2006

Real Estate agent schtick

While on the patrick.net theme (following), here is a terrific treatment authored by Patrick Killelea of how the real estate industrial complex convinces people to pay too much for housing: Housing Crash Continues, Bubble Pops

This free market rampage continues unchecked, unregulated and disregarded by our dodgy shyster politicians who pretend to be concerned about everything while doing absolutely nothing about anything.

As reader Sean Olender put it: "Many people have forgotten that their number one restriction on future freedom -- to do what they want, when they want, and to go where they want -- it isn't the Iraqis, or Iranians, or North Koreans, it isn't the axis of evil, it's their mortgage lender."

This free market rampage continues unchecked, unregulated and disregarded by our dodgy shyster politicians who pretend to be concerned about everything while doing absolutely nothing about anything.

As reader Sean Olender put it: "Many people have forgotten that their number one restriction on future freedom -- to do what they want, when they want, and to go where they want -- it isn't the Iraqis, or Iranians, or North Koreans, it isn't the axis of evil, it's their mortgage lender."

Thursday, December 28, 2006

Renters Gloat Over Housing Slump - Wall Street Journal

An article in the Wall St Journal concerning my good friend and fellow bubblebear Patrick Killelea, founder of patrick.net:

Renters Gloat Over Housing Slump - WSJ.com

Renters Gloat Over Housing Slump - WSJ.com

Sunday, November 19, 2006

The Coming Collapse in Housing

(click to enlarge)

When you look at Robert Shiller's graph of inflation of house prices, adjusted for monetary inflation, over the last 100 years, it seems almost inevitable that there will be a major correction very soon.

Of course, the politicians will just sit back and watch it rise and fall, so they can't be blamed for the outcome of 'irrational exuberance' (although they could be accused of indifference).

The Coming Collapse in Housing

Monday, November 13, 2006

Suffering in silence: a city on the edge of insolvency

Very interesting, NSW 'Labor'. The Joe Tripodis and Frank Sartors clearly really don't care what happens to the average household. The housing 'boom' is partly responsible for this, the subsequent inflation it caused has taken care of the rest.

Suffering in silence: a city on the edge of insolvency

ONE in three Sydney households is beset by financial worries and almost one in seven is teetering on the edge of insolvency, a church survey has found.

The study commissioned by the Wesley Mission warns financial stress is greatest in the south-west and outer west, but is also pervasive across all parts of the city, including its more affluent suburbs.

Families reported forgoing family activities, borrowing from relatives or friends, failing to pay bills on time or being unable to make minimum credit card payments.

Five per cent said they had had to pawn an item, 4 per cent said they had gone without meals and a similar number could not afford to heat their homes.

The survey of 400 people was carried out in August. Since then last week's interest rate rise - the third this year - has added $40 per month to average mortgage repayments.

Suffering in silence: a city on the edge of insolvency

Monday, November 06, 2006

Homebodies raise the drawbridge to avoid an out-of-control world - National

A telling sign of the times:

Homebodies raise the drawbridge to avoid an out-of-control world - National

IF THE home is our castle then we are raising the drawbridge.

Mounting frustration with the travails of modern life is driving us back into our homes, where we are seeking comfort in watching movies, eating and surfing the internet, a market research study has found.

The study on the mood of the nation by Australia SCAN found scepticism about business and government, a gloomy economic outlook and constant erosion of time and energy are leading to a sense of a loss of control.

Overall he noted a general malaise among the population, with more people less optimistic about the economic outlook and less confident of their personal finances than they were a year ago.

Homebodies raise the drawbridge to avoid an out-of-control world - National

Sunday, November 05, 2006

How could Sydney get it so wrong?

Then there's the thriving, hustling metropolis, where every opportunity to show intelligence or courage or (God forbid) altruism is mowed under the determined asphalt of commercial tackiness. Take the huge Carlton & United Breweries site on Broadway. Take Homebush and Rhodes Peninsula, spewing dioxins into the upper atmosphere in order to roll out more third-rate housing. Take Botany Bay, or Cooks Cove, or Green Square, or the vast tackiness spreading up and down the poor old Parramatta River. Take East Darling Harbour, our chance for a real flagship of eco-design, right at our ceremonial front door, now set to become more bottom-line junk, like King Street Wharf, only more, bigger, glassier. Most of them were, or are, Government land; all offered the opportunity for real social and cultural play. What do we get? More of the same.

This is a waste and a belittlement. A waste of our energies, as a city, and a belittlement of our intelligence and enterprise. To a large extent it is driven by the narrowness of our politicians, who talk tough but timidly follow the do-nothing-stay-in-power model of government perfected by Bob Carr and John Howard and become more philistine by the moment.

Blaming pollies is too easy. They're elected, and we elect them. If we wanted to make city-shaping issues into electoral ones, we could. We only have to be sceptical when they talk about conflict between the environment and job creation, and wonder how many jobs we'll have when the air turns to soup and the water laps at our doorstep. We only have to put our votes where our mouths are. We only have to find courage, take the risk, want to - enough.

How could Sydney get it so wrong?

Wednesday, November 01, 2006

Home ownership slips out of reach

Housing is at its least affordable in almost three years, with spiralling land costs and excessive fees making home ownership more out of reach for Australians.

"Since the national housing cycle hit its peak it has been readily apparent that the triple whammy of spiralling land costs, excessive fees and charges and planning red tape was making a tangible recovery in housing affordability virtually impossible.

"Moreover, a distinct lack of progress in addressing these three factors means that in the higher interest rate climate of 2006, we find ourselves back in the same affordability hole."

The manifest failure of government to act at any level on housing affordability in Australia simply beggars the imagination. It's so appalling that one begins to suspect a 1984-style conspiracy on the part of Ministers — "imagine a boot stamping on a face — forever".

Home ownership slips out of reach

Sunday, October 15, 2006

Sydney's pay-later poor

Sydney's pay-later poor The Sunday Telegraph

DEBT-stricken families with new homes, cars and plasma televisions in Sydney's sprawling housing estates are relying on charity handouts to buy food.

Welfare agencies report a worrying increase in the number of middle-income families with big mortgages seeking help to pay grocery, electricity and gas bills.

Dubbed the 'pay-later poor'' by St Vincent de Paul, they live in homes boasting cable television and the latest electrical goods and use credit cards to meet basic living costs.

Many of the families live in so-called McMansions.

Rising interest rates and petrol prices have hit them hard, with the latest figures showing soaring personal debt levels and bankruptcies.

Thursday, October 05, 2006

How the housing bust went west - Opinion - smh.com.au

Looks like the spruikers' stories caught the slower Westies out. When interest rates went to an all-time low, shrewd investors in the eastern and northern suburbs probably saw a price boom coming, and bought early, possibly to sell at the top. Once the seminar gurus got up steam and convinced the Westies to negative gear, because 'it always goes up', it was too late -- the tulip boom was busting.

Does the NSW 'Labor' government care about any of this? No way, they're too busy bailing themselves out of their countless screw-ups and aiding and abetting their capitalist cronies, many of whom are in property development themselves...

How the housing bust went west

Does the NSW 'Labor' government care about any of this? No way, they're too busy bailing themselves out of their countless screw-ups and aiding and abetting their capitalist cronies, many of whom are in property development themselves...

How the housing bust went west

Friday, September 29, 2006

We of the never-never home loans

THE RESERVE Bank is alarmed at the rise of interest-only home loans, warning of negative equity for borrowers who fail to make inroads into the principal of their loans while house prices fall.

Sydneysiders who bought at the peak of the property boom and have faced the sharpest falls in property values are most at risk of negative equity, where the size of the debt exceeds the value of the home.

Despite not having to make principal repayments, borrowers with interest-only loans were found to be twice as likely to fall behind on their payments. "The [nationally] higher arrears rate is hardly surprising, given the general lowering of credit standards that has occurred since the mid-1990s," the Reserve Bank said.

Fierce competition among banks for market share has led to an increase in interest-only loans being offered to people who previously may not have been considered creditworthy. A third of sub-prime borrowers - those who do not meet standard income or credit history requirements - choose interest-only payments.

But by lowering upfront repayments, these loans encourage already at-risk borrowers to take on more debt, the Reserve says.

Its review also found evidence that mortgage arrears are on the rise. NSW suffered the largest increase in loan arrears over the past year, consistent with other signs of stress, including a doubling in repossessions.

We of the never-never home loans

Sunday, September 17, 2006

Bought for $262,500 in 2003, sold for $95,000 last week

The boom is busting — a little. State and Federal govts do nothing to control such capitalist boom/busts based on irrational exuberance, of course, although, when you think about it, just about every single other aspect of property is controlled — what you can build, how high, how densely, to what standard, etc. Why do they let prices go free-floating to the detriment of the economy and individuals?

Bought for $262,500 in 2003, sold for $95,000 last week

Macquarie Bank property research analyst Rod Cornish said defaults among mortgage brokers and low-documentation loans were higher than major banks.

However, he said Australian Prudential Regulation Authority figures showed the number of loans across Sydney in default with the major banks had begun to rise.

'You would expect the price impact on homes would be worse in the outer western suburbs where the rates rises and fuel rises would have a higher impact,' he said.

Elliott Shiner First National real-estate principal Angela Elliott said: 'Everything that is selling now is selling for $40,000 to $50,000 less than it was in 2003. Properties have dropped by a good 30 per cent in value.

'You can pick up properties in the Mount Druitt area for $180,000 to $200,000. There are real bargains to be had, but where are the buyers?'

Bought for $262,500 in 2003, sold for $95,000 last week

Monday, September 11, 2006

PM told he's wrong on house prices

PM told he's wrong on house prices

Housing booms and unaffordability are multi-factorial. The Federal Coalition is as much to blame as anybody for keeping negative gearing on investment properties and halving the rate of capital gains tax – these are just two of the inputs to housing price increases. Other factors include liberalised credit products from lenders, low interest rates, a shaky share market, and the 'psychology of booms' or irrational exuberance. However, no government in Australia has done anything particularly meaningful yet to alleviate the housing boom or make life easier for first home buyers, but appear to be cheerleaders who want to join the club in uncritically celebrating every price rise as an 'increase in household wealth'.

Housing booms and unaffordability are multi-factorial. The Federal Coalition is as much to blame as anybody for keeping negative gearing on investment properties and halving the rate of capital gains tax – these are just two of the inputs to housing price increases. Other factors include liberalised credit products from lenders, low interest rates, a shaky share market, and the 'psychology of booms' or irrational exuberance. However, no government in Australia has done anything particularly meaningful yet to alleviate the housing boom or make life easier for first home buyers, but appear to be cheerleaders who want to join the club in uncritically celebrating every price rise as an 'increase in household wealth'.

Mr Robertson said the needs of first-home buyers were being ignored because most voters were home owners and therefore had an interest in higher, not lower, property prices.

'Neither the Coalition nor the Labor Party in Canberra show any sign of going out of their way to make any significant difference – [First-home buyers] are not a big enough priority for Canberra to do much beyond blaming the states for not releasing enough land,' he said."

Tuesday, September 05, 2006

Priced Out Of House And Home

The Register-Guard, Eugene, Oregon, USA:

There is one clear solution to the affordable-housing crisis: a real estate crash. It's the one housing issue that attracts media attention - because it would hurt the Owns. But while an easing of prices could be devastating for lower-income Owns with risky mortgages, it probably wouldn't bring home ownership within reach for many Own-Nots. Prices have too far to fall; in 2000, two-thirds of the home sales in Fairfax were for $250,000 or less, but last year, fewer than one-twentieth were. And even a modest price slump could trigger a construction slowdown that would make shortages of affordable housing for moderate-income families even worse.

Eventually, politicians may rediscover housing - not as an urban poverty issue, but as a middle-class quality-of-life issue, like gas prices or health care. Homeownership is often described as the American dream, but these days many workers would settle for a decent rental that won't bankrupt their families.

Saturday, August 26, 2006

Boom and bust on the home front - smh.com.au

The state government (ministers, advisers and sundry flacks), speculative investors, lenders, and voters should really have a good, hard think about this:

Boom and bust on the home front - National - smh.com.au

Of course, the PM is now suddenly worried about the problem of low housing affordability, whereas a few short years ago in a televised radio interview he shrugged, looked bemused, and said, "none of my constituents are complaining that their house values have gone up"... just another typical backflip from the PM...

Boom and bust on the home front - National - smh.com.au

Of course, the PM is now suddenly worried about the problem of low housing affordability, whereas a few short years ago in a televised radio interview he shrugged, looked bemused, and said, "none of my constituents are complaining that their house values have gone up"... just another typical backflip from the PM...

Tuesday, August 22, 2006

Home owners find equity a spent force

Tried to warn them:

Home owners find equity a spent force

THE stagnant property market has taken a toll on a favourite Australian pastime: converting bricks and mortar into cash.

The boom in equity withdrawn from housing and used to boost superannuation, bolster share portfolios and buy cars, overseas holidays and plasma televisions has petered out, a report by the Reserve Bank says.

Robert Mellor, of BIS Shrapnel, said Sydney house prices might fall a further 5 per cent this financial year because of higher interest rates, pushing more households into negative equity. However, the strength of the labour market was helping to prevent a surge in forced sales, he said.

Home owners find equity a spent force

Thursday, August 17, 2006

Consumer hopes dive as prices weaken pay rises

THE Coalition pinned 10 years of legitimacy on the fact that low and stable interest rates made for comfortable consumers. But mortgage pressure is rising everywhere and consumers have suffered the sharpest loss of confidence in 17 years.

So this week the Coalition dumped the political strategy of reassurance for a claim that it can manage adversity better than Labor.

The housing 'boom' chickens are coming home to roost...

Consumer hopes dive as prices weaken pay rises

Sunday, July 09, 2006

The Daily Telegraph | Suburbs' rent chaos

The Daily Telegraph | Suburbs' rent chaos: "SYDNEY'S rental crisis has spread west as outer suburb vacancy rates spark unprecedented competition among homehunters.

In some areas of Sydney desperate renters are panic bidding and offering to sign 18-month leases in an attempt to secure a home.

Other exasperated homehunters are so frustrated they have given up and turned to living in share accommodation with strangers instead."

In some areas of Sydney desperate renters are panic bidding and offering to sign 18-month leases in an attempt to secure a home.

Other exasperated homehunters are so frustrated they have given up and turned to living in share accommodation with strangers instead."